Critical Dependencies

How power consolidation of digital infrastructures threatens our democracies—and what we can do about it

By Michelle Thorne

Image credit: Anton Grabolle / Better Images of AI / AI Architecture / Licenced by CC-BY 4.0

About This Report

Stiftung Mercator commissioned Green Web Foundation to prepare a report aimed at philanthropic funders seeking to better understand how to strengthen the public’s interest in digital infrastructure at a systemic rather than symptomatic level. The report centers on recommendations to funders to understanding this topic and for further investments. It focuses on the following goals:

- Explain the importance of digital infrastructures to democracy by providing an analytical basis and taxonomy of issues. Emphasize the social, economic and environmental harms caused by unhealthy dependencies.

- Identify what we could learn from other fields dealing with complex debates about dependencies on infrastructure, such as climate and energy. Highlight successful approaches that challenge power consolidation and foster meaningful alternatives.

- Recommend pathways for funding of this topic with a focus on promising interventions in Germany and Europe.

Table of Contents

- Executive Summary

- Insights

- Recommendations

- Example Initiatives

- Positioning

- Overview of Digital Infrastructure

- Analysis of Harms

- Acknowledgements

- Footnotes

Executive summary

We are at an inflection point in digital infrastructures. There is much conversation about the unprecedented speed and scale of our computational future. Significant investments are being made, especially as part of private and national efforts to “win the AI arms race.” Meanwhile, more data is becoming available about the harms of these systems. No one has perfect knowledge of the situation, and in some instances, information is being intentionally obscured or distorted. Amidst the confusion and scramble, well-resourced players are seizing strategic footholds and advancing their cause. This moment is called the “fog of enactment.”1

Some of the wealthiest companies in the world spend billions in lobbying2, sponsoring research3 and building out parallel energy and digital infrastructures to further secure their market positions. Meanwhile, deliberative democratic processes take time and resources. The public and, at times, democratically elected officials lack access to the data and decision-making about our digital futures. Furthermore, the technical expertise to evaluate these tradeoffs from a public interest perspective is structurally under-resourced.

This report seeks to call out these maneuvers and recommend pathways for funding in the public’s interest with a focus on the energy and climate impacts of digital infrastructures and harms caused by current ownership models. We call for actions that are ambitious, collaborative and intersectional to help redistribute more power to the public interest and to just and sustainable digital futures.

Insights

Our findings emerge desk research, interviews with public interest experts and practitioners, and drew on our experience as a non-profit working on digital sustainability, open source, climate justice and digital rights. Later sections of this publication provide details and referencing. We find that:

- Digital resources — or the capacity to process, store and transfer data — are the foundation of our digital economy. The entities best positioned to generate digital resources profit the most from the growth of the digital realm. Such companies use bundling, regulatory capture and inoperability to run closed markets which are not transparent and lock-in customers. They capitalize on and intensify society’s growing dependences on digital resources as they fuel demand for digitalization and high intensity computing such as AI systems. This dynamic further consolidates their market power, making it difficult for new entrants and enabling the same companies to expand their control over more sectors such as energy.

- The goals of democratic societies are not the same as the goals of the wealthiest companies on earth. While democratic societies need and want digital products and services, such as meaningful connectivity, this is not the core business model of these companies. A closed digital infrastructure market intensifies inequalities and stifles competition and innovation while under-delivering on the basic services society needs.

- Many digital infrastructures suffer from a democratic deficit. Impacted communities are alienated from the information and decision-making process about the costs and benefits of digital infrastructures. Nevertheless, they are made to bear the burden of their harms.

- Democratic participation should help determine the purpose digital infrastructures and how resources are allocated to them. This practice could address the democratic deficit of our current ownership models. However, this requires alignment and shared rules across territories, so that one community’s victory does not displace the conflict and shift the harms to another community. The community energy sector can provide useful patterns.

- Funding is vastly asymmetrical and current fiscal policies entrench these disparities. The richest companies in the world are buying and building the energy and computer systems at unprecedented rates with state subsidies.4 Meanwhile civil society scrambles to find scarce resources to articulate and mitigate harms. Foundational democratic commitments as deprioritized, such as meaningful internet connectivity and emissions reduction targets for the digital sector, in favor of technological hype. This leaves a resourcing gap for deep, sustained and intersectional public interest infrastructure.

Recommendations

These recommendations are aimed at philanthropic funders seeking to better understand how to strengthen the public’s interest in digital infrastructure at a systemic rather than symptomatic level. It focuses on the unique role that philanthropy plays in contrast to funding from the public and private sectors. We favored recommendations that go beyond maintaining the status quo and efficiencies and instead focused transforming underlying structures towards more equitable outcomes and restoring ecosystems, inspired by the regenerative model from the architect Bill Reed.5 This perspective is also informed by funders and practitioners working intersectionally and supporting a broad theory of social change we describe as “move slowly, quickly.”

- Diversify the production of digital resources by strengthening competition law, interoperability, and unbundling cloud providers. Digital resources6 form the baseline unit of the digital economy, and the major cloud providers are the main producers of these digital resources. In Europe, almost ¾ of the overall cloud computing market is controlled by three companies: Microsoft Azure, Google Cloud, and Amazon AWS.7 These companies, headquartered in the United States, undertake extensive maneuvers to reduce their taxes in the European countries in which they operate.8

Although they face multiple anti-competition cases, these companies generate ample cashflow thanks to their vertical integration and core business models (advertising, licensing and e-commerce). This profit in turns enables them to build more infrastructure. By controlling the infrastructure that underpins the digital economy, they position themselves to uniquely profit from digitalization—be it societally useful or not. The Digital Markets Act seeks to address some monopolistic practices. However, the integrated infrastructure business units (‘their cloud business’) are outside the scope of this regulation and more work is needed to break up this power concentration. - Advocate for digital infrastructure that serves the public good and operates within planetary boundaries. Current projections of AI growth show that energy demand for high intensity computation will outstrip what national decarbonizing grids can provide.9 All major digital infrastructure operators purchase significant renewable energy and add new generation to the grid. However, this new generation is largely meeting their own private new demand rather than decarbonizing the grid for pre-existing demand.10 This gap in renewable energy generation means that households and other sectors have to rely on fossil fuels while digital infrastructures are prioritized with green energy.11 National digital strategies should address how digital infrastructures will operate within planetary boundaries while also providing universal basic digital services, such as meaningful connectivity, for all who want it. Providers of digital infrastructure should face a burden of proof that the resources going to their systems are benefiting the public good and meeting environmental and climate targets.12

Here are opportunities to connect with research exploring how digital technologies can reduce harm to environmental ecosystems and help cut emissions to hit life-preserving climate targets. Nevertheless, these approaches must be grounded in the realities of the natural resources available, include democratic processes and oversight and move away from false solutions and green extractivism13 so as not to perpetuate, perhaps inadvertently, harm towards frontline communities.14 - Defend and support independent research into the harms of digital infrastructure companies. Tech companies often obstruct and undermine the public’s knowledge of their operations and impacts. For example, they forbid access to researchers who try to work independently or increasingly use lawsuits and other forms of legal harassment to intimidate them. Large digital infrastructure companies are notorious for not providing information that exposes their cost structure.15 Transparency is an important step. The European Corporate Sustainability Reporting Directive (CSRD) will help gain access to data about the finances and sustainability of companies. Furthermore, an attempt was made by the EU within the Energy Efficiency Directive to implement minimal transparency efforts. But this law does not guarantee public access to the environmental impact.

Yet much more is needed on top of that transparency. From human- and machine-readable ways of navigating public reporting data16 to stronger enforcement and compliance, as well as independent research to contextualize and deepen these results. - Strengthen democratic participation in decision-making about digital infrastructures. Democracy is sometimes described as a muscle: if it is not exercised, then it atrophies. Citizens and impacted communities are often shut out of decision-making processes about where and how these infrastructures are built and maintained, who benefits from them and who carries the burden of harms. To address the democratic deficit in digital infrastructures, communities must be involved in meaningful ways to foster their digital self-determination and ensure their voices are heard as a counterweight to industry lobbying. The research institute AI Now suggests that companies be required to affirmatively demonstrate that they are not doing harm as opposed to asking the public and regulators to continually investigate, identify, and find solutions for harms after they occur.17 In the rooms where decisions are made about digital infrastructures, we must ensure there is public interest representation. This requires sustained funding and cultivating a community of practice to use those moments effectively.18

Other important approaches include strengthening the multistakeholder model in spaces such as the UN Internet Governance Forum, which is currently under threat from authoritarian control and is shutting out civil society,19 and fostering worker representation on companies’ governing bodies.20 - Invest in digital self-determination and alternative imaginaries. What does it look like if digital resources are generated and stewarded by communities rather than corporations? Central to democracy is choice — the agency and the ability to make decisions about one’s life. In democratic societies, our digital infrastructures should support our self-determination, even if the decision is to opt out of these infrastructures. Increasingly, our choice of digital infrastructure is limited, let alone opting out of them completely. It is critical to have the possibility of choosing and for these alternatives to be viable. There must be genuine choice than, for example, choosing between two nearly identical hyperscalers. Public interest investment into imagining and building these alternatives is critical.

Other sectors have established patterns for community ownership.21 Successful examples include community energy where for the last 30-40 years, growth in energy in Europe has come from community energy projects, led by countries such as Germany and Denmark.22

Monopolistic digital conglomerates are not special — just new. There are patterns from other eras and other sectors for addressing the lack of democratic participation and public interest representation in infrastructures. But these changes won’t happen without proactive funding. Philanthropic funding is well positioned to resource a deep bench of people working on these issues in a sustained way so that there is the capacity to challenge and change the systems.

Public interest policy moves beyond a narrow focus on legislative and policy levers and embraces a broad-based theory of change. Funders must bring together more groups trying to climb the mountain from different sides. Unlike the private sector, philanthropy can help identify alliances across social movements and advocate for solutions that co-benefit impacted communities and the planet. And in comparisons to government funding, philanthropy can be more agile and intersectional. Regardless of funding mechanism, the scale and urgency of the crises call for investments must be ambitious, intersectional and towards regeneration.

Example Initiatives

To provide more concrete examples of what these recommendations could look like in practice, we gathered several example initiatives. The purpose of this list is not to be exhaustive but illustrative.

- UNBUNDLE THE BIG TECH CLOUD

There is an opportunity to explore more disruptive policies to break up digital infrastructure monopolies, such as the mandated unbundling of large digital product and infrastructure conglomerates.23 This move could reign in anticompetitive behavior among cloud providers, such as their service and resource bundling, high exit-fees for leaving their markets and inoperability. This example takes inspiration from successful patterns in other sectors such as the liberalization of the energy market—which solved both the market interoperability and exit fee (‘openness’). Efforts here could focus on unbundling these conglomerates so that the cash-generating core business (ecommerce, advertising, licensing amongst others) is separated from the infrastructure business. Funders could, for example, support the exchange of expertise and drafting of public interest strategies that build on precedence set in other sectors such as energy24 as well as support public interest technology think tanks in Europe25 to further develop and advocate for these changes. - GREEN UNIVERSAL CONNECTIVITY FOR ALL BY 2030

Several UN bodies have committed to targets to achieve universal connectivity by 2030 (UN Secretary-General’s Roadmap for Digital Cooperation,26 ITU Connect 2030 Agenda27). The UN Human Rights Council furthermore passed a resolution in 2021 which calls for “the promotion, protection and enjoyment of human rights on the Internet”28 and further reinforced state commitments to enhancing Internet accessibility and affordability and the objective of universal access.” There is an opportunity to pair these calls for universal connectivity with targets to reduce the emissions generated from the internet and transition digital infrastructure away from fossil fuels by 2030.29 In this way, internet connectivity could be positioned as essential for democratic societies while also needing to operate within planetary boundaries.30 - THE COALITION FOR INDEPENDENT TECHNOLOGY RESEARCH

Independent research is critical to ensuring that the public has trustworthy information about digital infrastructures and policymakers can make data-informed decisions about the regulation and more. Groups like the Coalition for Independent Tech Research advocate for transparency while also making the case for the public to understand how digital platforms and digital infrastructures shape society. Unfortunately, the increasing regulatory scrutiny that companies in the digital economy are facing has led to an increase in aggressive actions towards independent researchers. This is a trend present throughout the history of industrial revolution from oil to tobacco to chemicals—and which our field is underequipped to tackle. Efforts to strengthen resiliency of the field, through strategic communications, affirmative and defensive litigation strategies and cross-sector organizing, are essential to ensure that the foundation of evidence on which good regulation rests does not crumble. - INTERNET CITIZEN ASSEMBLIES

This example follows the success of citizen assemblies31 on other issues such as climate action and reproductive rights.32 Democratic fora could be held locally and regionally for a representative selection of people to conduct a genuine deliberation, hear from experts and frame referenda and other actions that determine the future of digital infrastructures in their communities. Possible topics could include participatory budgeting wherein citizens prioritize how finite resources such as land and water are allocated to different kinds of computation take place in their communities. Such an approach would yield more robust civic conversations about the tradeoffs of digital infrastructures in tangible and direct ways. - SOVEREIGN TECH FUND

The Sovereign Tech Fund supports the development, improvement and maintenance of open-source software. Its goal is to sustainably strengthen the open source ecosystem. It focuses on security, resilience, technological diversity, and the people behind the code. There’s a particular emphasis on digital services in the public interest (digitale Daseinsvorsorge). This is described as the responsibility of the government to provide digital services, and goods to ensure long-term access, equal living conditions, and protect an individual’s sovereignty in a digitalized society. Supporting this fund and encouraging other governments to create similar mechanisms would greatly benefit the public. - GREEN SCREEN COALITION FOR DIGITAL RIGHTS AND CLIMATE JUSTICE

The Green Screen Coalition works to catalyze exchange across the digital rights and climate justice movements. It originates with funders in open source and public interest tech who set out to learn about how their strategies intersect with climate and environmental issues. They identified that climate and technology share important features: complexity, disparate impact on communities, and a meaningful impact on how we will experience the future. Holding this complexity requires funders to be thoughtful in their investments and actions, accelerating the use of existing and emerging tools that can empower communities and conservation efforts, while also constraining the potential for harm from false tech “solutions”. Using peer learning and pooled funds, the Green Screen Coalition is investigating how to take investments beyond siloed interventions and into more powerful, structural change. This includes the commitment to funding ecosystems and prioritizing most impacted people and areas and working with an intersectional lens.

Positioning

“Technology, power and democracy. All three of these topics have been studied since Aristotle without decisive conclusions. If we combine them today, there’s still no eureka. Nevertheless, when I think about the concentration of power we’re experiencing today, Europe has been here before—facing challenges from consolidated communications infrastructure. I am hopeful because there are many patterns and precedents for action.”

Dr. Niels ten Oever

Co-principal investigator, critical infrastructure lab at the University of Amsterdam

“There is something different about this particular moment: it is primed for action. We have abundant research and reporting that clearly documents the problems with AI and the companies behind it. This means that more than ever before, we are prepared to move from identifying and diagnosing harms to taking action to remediate them. This will not be easy, but now is the moment for this work…[to] meaningfully confront the core problem that AI presents, and one of the most difficult challenges of our time: the concentration of economic and political power in the hands of the tech industry—Big Tech in particular.”

Amba Kak and Sarah Myers West

“AI Now 2023 Landscape: Confronting Tech Power,” AI Now Institute, 2023

This report seeks to contribute to the conversation about the consolidation of power in our digital infrastructures and the harmful dependencies it creates. Building on existing analysis from scholars, activists, practitioners and funders, we aim to understand the underlying drivers of these harms and uplift promising work already underway to combat these problems and advance the public’s interest.

As a non-profit headquartered in Berlin, we focused on the dynamics of digital infrastructure in the European Union with an emphasis on Germany and its data center clusters in the Frankfurt/Main region and Berlin-Brandenburg. Our findings are informed by applied research from our organization on digital sustainability and the use of open source tools as an accelerator to shift digital infrastructures off of fossil fuels. We are active in industry consortia, such as the Green Software Foundation which convenes some of the largest cloud providers to discuss how to measure and mitigate emissions from digital services. We also co-founded the Green Screen Coalition to learn alongside funders and practitioners how to build bridges across the digital rights and climate justice movements. In this report as in our other work, we strive to listen to perspectives from most affected areas and people and to acknowledge our privileges as primarily white, English-speaking, tech-literate citizens from the minority world.

We also sought to address the rising energy demand from AI systems in countries such as Germany that are trying to decarbonize their electricity grids while under heavy lobbying pressure from the cloud providers that sell these AI systems. We express concern that the “AI arms race” is further consolidating power and locking societies into systems that are undemocratic and unsustainable while alienating communities and extracting value from their data and finite natural resources.

We also advocate for universal internet access and meaningful connectivity. Digital infrastructures are necessary to provide internet connectivity, as well as data storage and processing capacity. They have become an essential utility—analogous to electricity in the industrial era. We must treat this new utility with caution, as it is leading to monopolies that constrain the market for digital infrastructure and hinders competition and innovation and is resulting in unprecedented wealth consolidation. Nevertheless, history shows us that these sectors can be regulated. The electricity grid today benefited greatly from breaking up these monopolies and investing in alternatives, including community energy. This precedence gives us hope for the digital sector.

Overview of Digital Infrastructure

This section introduces an analytical framework for understanding digital infrastructures from a systemic perspective. It expands on that definition by describing the powers that control digital infrastructure today in Europe and Germany and concludes by explaining how this power consolidation hinders competition and identifying some of the governmental bodies responsible for addressing the future of digital infrastructure.

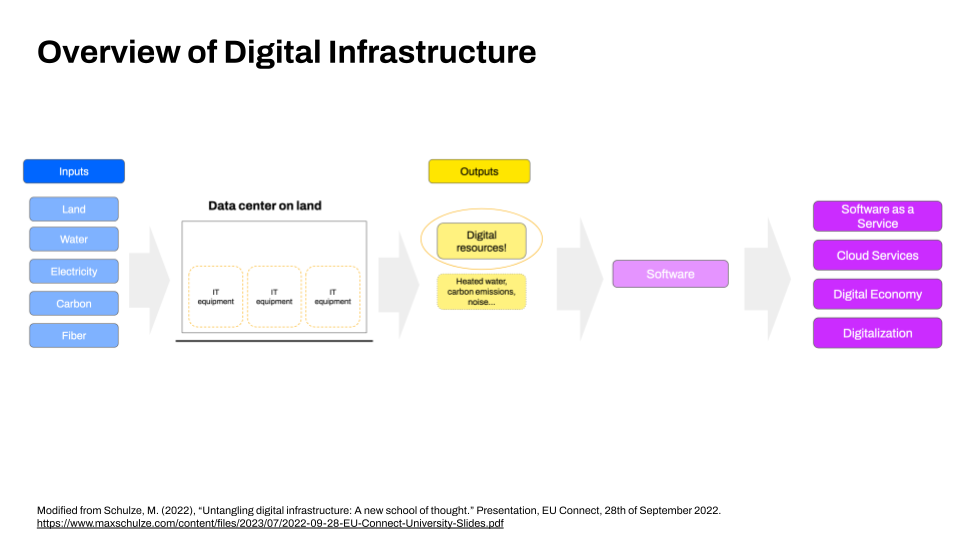

1. What is digital infrastructure?

| Digital resource | The base unit needed to make software. Digital resources are used to create digital products. |

Digital product | We refer to a “digital product” as a product that only exists in virtual form, for example software as a service. Digital products are often used to transform non-digital things into digital ones, and they therefore require digital resources to work. Compare this to “digitalization,” which is about transforming existing (often physical) products by integrating digital capabilities, such as a car running on a software operating system. |

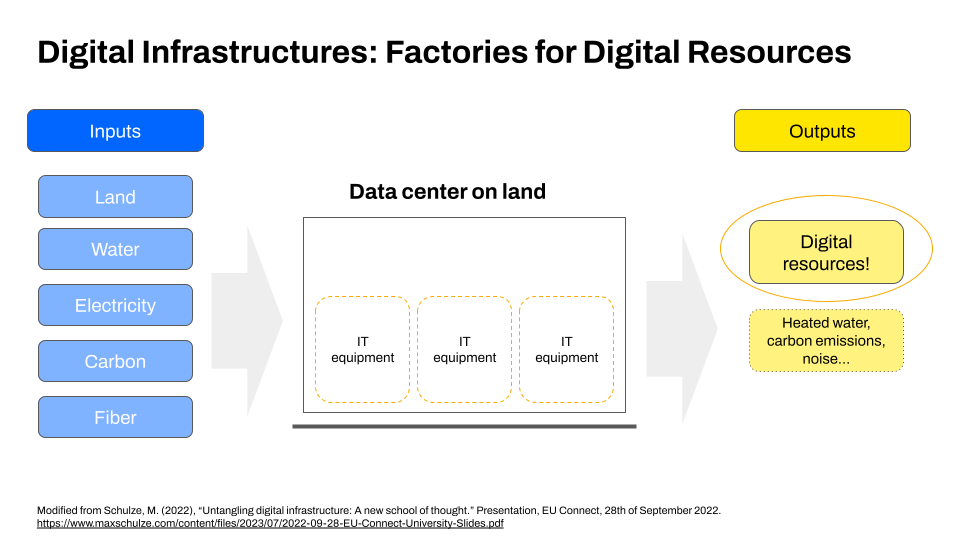

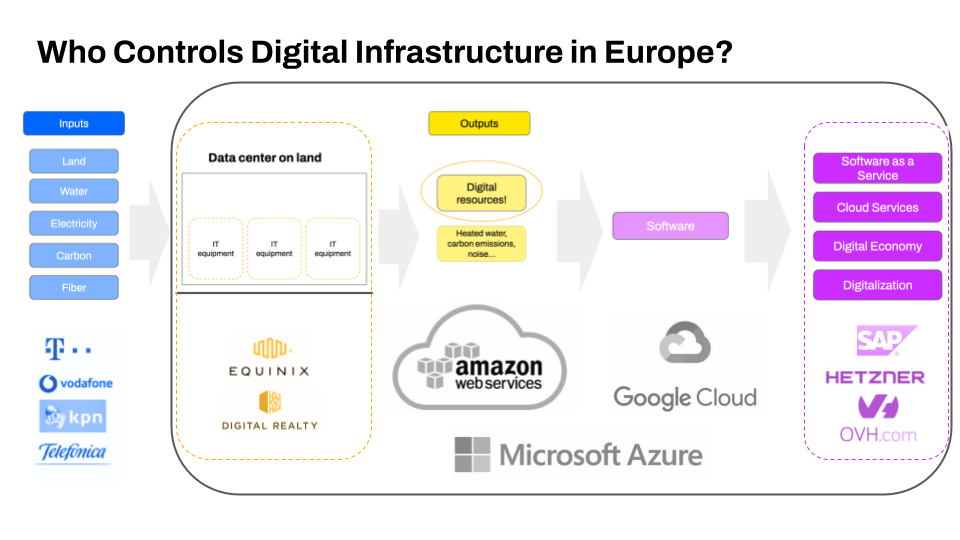

Digital infrastructure | The means of production of digital resources. Digital infrastructure is the “factory” that generates digital resources. It’s usually a data center on a piece of land that relies on electricity, water, connectivity and other resources as inputs. These inputs are plugged into servers and other IT infrastructure to transform these materials into digital resources. Owners of digital infrastructure are in the business of generating digital resources. They use the digital resources they make to power their own products, or they sell the resources to clients. |

We use the term digital infrastructure to describe the means of production of digital resources. We cite the above definitions of digital infrastructure from the Sustainable Digital Infrastructure Alliance (SDIA)3334 because they articulate how value is extracted when natural resources are transformed into digital resources. In the SDIA model, the data center is described as an empty factory. It takes inputs such as land, water, electricity, carbon emissions and fiber, and then within a cooled office building filled with servers and computers (a “factory”) these inputs are transformed into digital resources, alongside waste and other outputs including heated water, carbon emissions, noise and more.

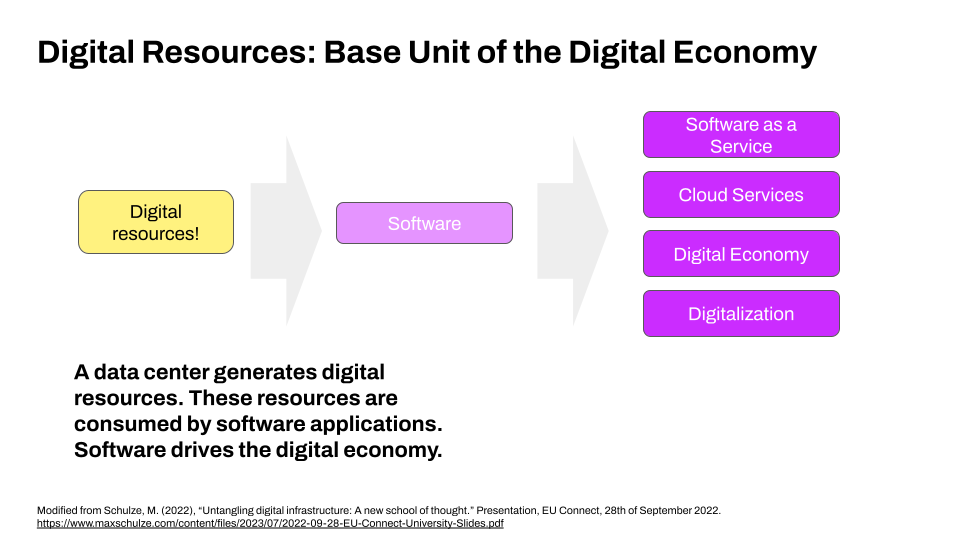

These digital resources form the base unit of our digital economy. They represent the capacity to process, store and transfer data. Software applications consume these digital resources and transform them into in any number of digital products, such as cloud computing, storage products, networking, software as a service, cryptocurrency mining and increasingly AI computation.35 Without digital resources, software doesn’t work.

2. Who controls digital infrastructure in Europe?

The entities best positioned to generate digital resources control the market and profit the most from digitalization. For this report, we focus primarily on digital infrastructure businesses of large, global digital conglomerates and their connectivity, data centers and infrastructure services because they operate as an unregulated monopoly with transnational impact and vertical integration through their conglomerates that enables them to have an outsized influence on other sectors such as energy and land.

The top three infrastructure business units, Amazon Web Services, Microsoft Azure, and Google Cloud control almost ¾ of the overall cloud computing market at the close of 2023.36 The cloud computing market is expanding year on year and consistently benefits the very same infrastructure providers. In France, for example, the triopoly comprised 80% of the growth in public cloud infrastructures and applications expenditure in 2021, prompting the national competition authority to caution against anticompetitive behavior.37

Digital infrastructure operators rely on land, water, electricity, fiber and other inputs to generate digital resources. Therefore, it is helpful to monitor trends in data center and fiber-network construction to understand the scale of investments and who controls them.

In the last five years, the total number of data centers globally has doubled. There are nearly 1000 active hyperscale data centers worldwide (> 50 MW of installed electrical capacity) with over 400 additional facilities publicly announced. Within the next five years, the biggest conglomerates are anticipated to control over half of all data center capacity38— with nearly 50% of that capability being “own-built, owned data centers.”39

This trend in digital infrastructure is significant. Amazon Web Services, Microsoft Azure, and Google Cloud will increasingly produce digital resources in self-constructed, self-managed, fully owned and integrated data centers, marking a shift from previous reliance on shared facilities that usually cater to a more diverse client base.40 Because the conglomerates increasingly own their data centers, they are positioned to gain immensely from soaring demand for digital resources, especially from high-intensity computation using large language models and other generative AI services that run on data centers’ digital resources. Amazon’s AWS, for example, will hit $100 billion in revenue in 2024, and they attribute much of their increased profit because of workloads being moved to the cloud.41

While European cloud providers do grow alongside the general market growth, their share dwindled from 27% to 13% in 2022.42 SAP and Deutsche Telekom are the biggest European cloud providers, individually holding 2% of the regional market share, and other European companies such as IONOS, Hetzner, OVH, and Leaseweb play an important role as infrastructure providers that use different business models than the conglomerates.

The annual cloud computing market globally is estimated to soon reach the $500 billion mark.43 The European cloud infrastructure market size was valued at €15.3 billion in 2021 with projections of market growth to approach €100 billion by 2026.44

The German cloud computing market was valued at €10.3 billion in 2020 and is expected to grow 15-17% from 2021 to 2028. The biggest cloud providers in Germany are Microsoft Azure, Google Cloud, and Amazon Web Services. As of 2021, Microsoft Azure held around 30% of the German cloud market share, followed by Google Cloud with approximately 20% and Amazon Web Services at 15%.45 Furthermore, the same leading cloud companies are building and paying for priority access to energy infrastructures and strategic land assets to ensure steady and affordable access to electricity and other key inputs, so that they can continue to generate digital resources and make a profit.

In terms of capital invested in digital infrastructure, it’s important to note the size of the telecommunications and networking. Estimates range from a €220 billion European market with Germany spending the most at €41 billion for telecom infrastructure.46 While telecommunications play an important role in the digital infrastructure “stack,” countries like Germany have several different players meaningfully active in the market, including Deutsche Telekom, Vodafone Group, Telefónica Deutschland, and KPN.47 Combined, these companies control approximately 78% of the German telecommunications market with Deutsche Telekom leading at around 40% as of 2022.48 For data center networking, the market in Germany is valued at around $1 billion and is expected to grow annually around 5%. Digital Realty is cited as the market leader for data center networking in Germany with a 19% share.49

Important to keep in mind about infrastructures is the timescale of their planning, construction and usage. Infrastructure decisions today take decades to be realized. For example, energy transmission lines take 10-15 years to plan, construct and bring into full use.50 Data centers operate on 20-year time horizons. Tech companies typically sign power purchase agreements for up to 30 years. For Germany, Bitkom estimates that the capacity of data centers in Germany will double by 2025 and that Berlin will join Frankfurt as the most important data center cluster in the country with several large facilities in the pipeline.51 While most philanthropic funding works at one-to-five-year grant cycles, data center regulations today can influence decades of construction. Longer-term thinking and resourcing are required when seeking to affect the trajectory of digital infrastructures.

3. Dynamics in the cloud

“Incumbents that control key inputs or adjacent markets, including the cloud computing market, may be able to use unfair methods of competition to entrench their current power or use that power to gain control over a new generative AI market.”

US Federal Trade Commission, 202452

Here we will focus on the companies who produce digital resources in a consolidated market, namely the cloud providers. The European cloud market suffers from high barriers to switching providers, which constrains new players when competing for customers from established companies.53 The market for digital resources in Europe and Germany is increasingly closed and anticompetitive. Highly concentrated power, plus anticompetitive tactics, hinder entry from European small and medium businesses, and growth prospects in the business of providing digital infrastructure.

Digital infrastructure owners, and cloud providers in particular, hold their market position with a variety of tactics. Competition authorities in the USA, France and UK independently raised concerns about the following practices:

- Egress fees (‘exit fees’) which are fees paid if you move your data out of their service. The leading cloud providers set very high fees, deterring customers from switching or using multiple providers.

- Technical restrictions on interoperability and bundling of services & resources restrict compatibility between services offered by different providers, which locks in customers or makes them jump through hoops to use alternate providers.

- Free credits that incentivise consumption and committed spend discounts create an incentive to rely on a single cloud provider, making it less viable for customers to switch if needed.54

- Overproducing digital resources so that they can offer computation at a lower price and create anti-competitive pricing.55

The above barriers as well as established customer bases, brand recognition, abundant financial resources, and political clout render it difficult for smaller firms to enter the market and compete effectively, thus hindering innovation around costs and environmental impact. These dynamics also influence the control of other technology markets such as AI systems, which are highly dependent on accessing digital resources at low costs.

EU Digital Markets Act. The European Union has taken important steps to challenge this gatekeeping, especially with the Digital Markets Act. However, it still leaves a gap in addressing the anticompetitive dynamics in the cloud computation landscape, for example in not adequately overseeing certain kinds of software.56

Unlike many other sectors where there are savings made with infrastructure, the financial benefits are not passed onto customers of digital infrastructure. For example, savings from carbon-aware data processing on the customer side are harvested by the infrastructure provider who captures the savings by selling the energy back to the grid rather than rewarding the customer. This is in contrast with, for example, the energy sector and its electric vehicle tariffs, that incentivizes customer efficiencies and passes those savings on to them.

Analysis of Harms: Climate & Environment

Here we build on the definition of digital infrastructure and illustrate how monopolistic control has intensified extractivism, pollution and rising emissions as well as water consumption. We focus on how these dynamics impact European populations, especially in Germany, and how these negative environmental impacts are projected to intensify with the increased adoption of AI systems. We look to other infrastructure sectors, such as energy, for solutions to these challenges.

4. What are the climate and environmental impacts of digital infrastructure in Europe?

Digital infrastructure in Europe contributes significantly to greenhouse gas emissions (GHG) and resource consumption, especially water, as well as localized impacts such as air and noise pollution.

Energy and GHG emissions

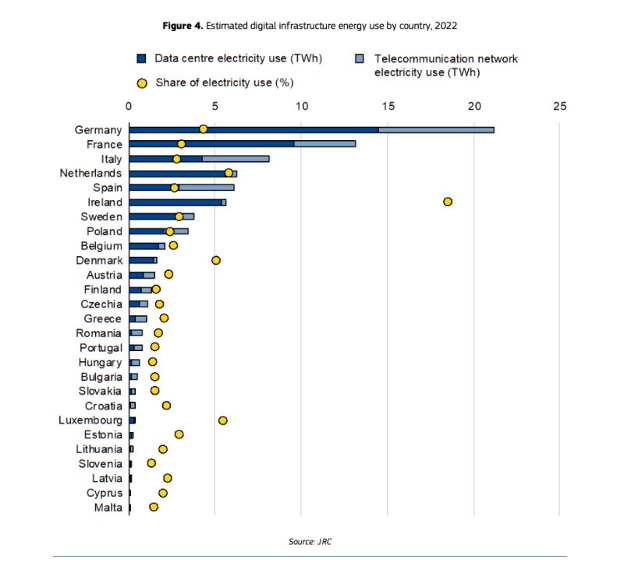

Data centers worldwide are responsible for 1-3% of global energy-related GHG emissions (around 330 Mt CO2 annually), mainly due to the massive energy demands required to maintain server farms and cooling systems. These emissions are more than the aviation industry.57 Energy demand for data centers has increased substantially year on year, growing by 20-40% annually. In the European Union, data center electricity consumption was estimated around 100 TWh in 2022, almost 4% of total EU electricity demand. By 2026, forecasts indicate that it will reach almost 150 TWh, a third more than in 2022.58 In some European countries such as Ireland and Denmark, data centers already use a fifth of the countries’ total electricity consumption.59

The International Energy Agency (IEA) reports that the combined electricity used by Amazon, Microsoft, Google, and Meta has more than doubled between 2017 and 2021, rising to around 72 TWh in 2021. Notably, the IEA also argued, “To get on track with the [Net Zero Emissions] Scenario, emissions must halve by 2030.”61 The ITU similarly recommends halving emissions by 2030 and an annual decrease of 4.2%.62

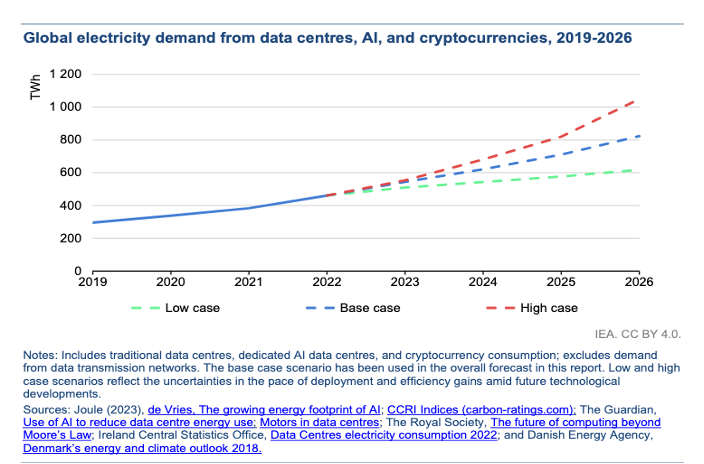

AI and cryptocurrencies are projected to require “160 TWh up to 590 TWh of electricity demand in 2026 compared to 2022, roughly equivalent to adding at least one Sweden or at most one Germany.”63 The IEA has further highlighted this trend from AI and cryptocurrencies as one of the more significant drivers of global demand of electricity.64

Water

Closer investigations into the materiality of data centers, in particular their water consumption, were ignited in the 2010s after it was revealed that sites such as the NSA’s processing center in the drought-prone state of Utah uses millions of liters of water a day.65 Data centers continue to consume massive amounts of water first directly for cooling, in some cases sourcing 57% from potable water and indirectly through the water requirements of non-renewable electricity generation.66 Water consumption tends to be less transparent than energy usage—with less than a third of data center operators measuring water consumption. Nevertheless, freshwater usage is included in EU and national legislation, such as the EU Energy Efficiency Directive and the new German Energy Efficiency Act (EnEfG), with requirements to report. However, there is no legal obligation to reduce water use a level that does not deplete the water table to the extent that it prevents other uses.67

Water consumption trends are intensified with AI. Recent research from the University of California revealed that training GPT-3 in Microsoft’s state-of-the-art U.S. data centers can directly evaporate 700,000 liters of clean freshwater, but such information has been kept a secret.68 The same report anticipates the global AI demand may be accountable for 4.2 – 6.6 billion cubic meters of water withdrawal in 2027, which is more than the total annual water withdrawal of Denmark or half of the United Kingdom.

Waste and pollution

In addition to the consumption of energy and its associated emissions, it is well established that manufacturing and disposing of electronics used in digital infrastructure generates substantial waste and pollution which severely impacts the health of people near those sites.6970717273 These negative health and environmental impacts are experienced disproportionately by communities in the Majority World, continuing the practice of environmental colonialism.74

5. Where is digital infrastructure being operated to the detriment of communities and ecosystems?

Wherever digital infrastructures are built and operated, they impact local communities and ecosystems. Water, for example, is a critical issue when looking at digital infrastructure. Countries like Spain face severe droughts with reservoir levels dropping to historically low levels. This scarcity has brought attention to the substantial water consumption of data centers which use millions of liters daily for cooling purposes, in some cases 57% sourced from potable water.75

Water shortages in Germany

Germany is one of the regions with the highest water loss worldwide.76 As extreme weather events and droughts become more frequent due to climate change, the tension between data centers’ water needs and the finite water resources in Germany will grow. Meanwhile, responsible local authorities in Germany often do not know how much groundwater is available for them to distribute. In the Frankfurt area, which houses the largest cluster of data centers in Germany, water has been pumped from a nearby forested region to the city for decades. As a result, the forests in the Rhine-Main area are among the stressed hotspots in Central Europe, and the water reserves are so overused that the ground gives way.77 Berlin-Brandenburg is another water stressed area in Germany, and the region is on track to become the country’s second data center hub with a very large facility in Lichtenberg78 and Google’s forthcoming data center on the outskirts of the city.79

Green extractivism in Ireland

The case of Ireland is particularly noteworthy where data centers are expected to use nearly 30% of the country’s electricity by 2028.80 Rural environmental struggles are accelerated by the data center industry and postcolonial regimes, offering up the country’s natural resources for extraction on unfair terms.81 Importantly, after a campaign by civil society to address this issue, the Irish utilities regulator announced a limitation on data centers around Dublin. The campaign’s organizer argues that the construction of data centers needs to adhere to democratic standards so that they could benefit communities rather than powerful companies, and to do so in a sustainable way.82

Sites of struggle in the Netherlands

As researcher Dr. Fieke Jansen from critical infrastructure lab at the University of Amsterdam explains, “Data centers are sites of struggle”83 in the Netherlands and beyond. Citizen campaigns like Save the Wieringermeer84 opposed the construction of two Microsoft data centers. Their concerns included impacts to local agriculture, excessive water and renewable energy usage, water pollution and the release of heat to the air. To make matters worse, when the costs for electricity are skyrocketing, the hyperscale data centers are reported to receive significant discounts on their net tariffs.85

Jansen argues:

“[The struggle over land, water and energy] are very much governance and decision-making issues. Residents and civic actors feel that they are either not heard or ignored in zoning plans, environmental visions and area plans. This is not surprising when we look at the different forces at play for bringing a new industry to a specific location. The window of opportunity to influence decision-making happened long before the public became aware of the plans to build the data centers.”

6. How will resource consumption and local impacts evolve as demand for digital infrastructure and AI increase?

The surge in demand for digital infrastructure driven by AI applications will amplify resource consumption and local impacts if preventive measures aren’t implemented. Rapid expansion of digital infrastructure to support AI workloads will lead to escalating energy consumption, land use, water withdrawal, and e-waste generation.86 Moreover, AI models’ training phase, particularly deep learning algorithms, consumes enormous computational resources,87 generating significant carbon emissions.88

In terms of digital infrastructure, recent generative AI advances will “not so much to increase the number of data centers—which will continue to grow by well over a hundred per year—but to substantially increase the amount of power required to run those data centers.”89 That is because the number of GPUs in hyperscale data centers is skyrocketing with generative AI’s computational demands. As mentioned elsewhere, water will be a critical issue for these infrastructures. The impacts of water consumption are not an engineering problem to be solved but rather a question of environmental justice and democratic participation. Dr. Theodora Dryer’s work on water justice and technology outlines these dynamics with many case studies in the US.90 Similar research should be conducted in Europe and Germany specifically, given the strain on the country’s water and the heavy investments in digital infrastructure.

Analysis of Harms: Social

In this section, we summarize how monopolistic control of digital infrastructures is exacerbating social inequalities. We argue for prioritizing meaningful connectivity over technological solutionism. Here again we look to the energy sector for alternative ownership models such as community energy.

7. How are the harms and benefits of digital infrastructures distributed?

The distribution of harms and benefits from digital infrastructures in Europe and Germany follow existing social and economic disparities and further reinforce inequality. Marginalized groups, rural populations, and lower-income households generally face greater difficulty reaping the rewards of digitalization91 while simultaneously bearing the brunt of privacy violations, discriminatory algorithms, misinformation, and surveillance. As we know from intersectional and systemic analysis from public interest groups like Digital Freedom Fund, marginalized people suffer disproportionately from structural vulnerabilities perpetuated by opaque corporate policies and inadequate legal safeguards.92

These asymmetrical patterns undermine the democratic vision of inclusive, equitable societies. Bridging this divide requires engaging in affirmative policies aimed at redistributing wealth, fostering digital literacy, strengthening regulatory oversight, and providing meaningful internet connectivity for everyone who wants it.

The monopolization of digital infrastructure in Europe leads to missed economic opportunities as well. Consolidating power among a few dominant actors results in decreased innovation and restricted economic opportunities for citizens and businesses.93 By concentrating decision-making authority in the hands of a few entities, monopolistic dynamics limit the emergence of novel ideas, techniques, and services, and diminish the potential for widespread participation and inclusion.94 Monopolization further impedes societal welfare by inhibiting the free flow of information, obstructing fair competition, and compromising users’ privacy rights. Policies advocating for openness, plurality, and decentralization can counter these forces.95 To reiterate, the financial beneficiaries of monopolized digital infrastructure are the major US tech companies. Of the top ten wealthiest companies in the world, across all sectors, eight of them build and maintain hyperscale cloud services, provide AI services or the underlying chips and semiconductors to power them.96

As the AI Now Institute points out, “There is no AI without Big Tech…A core attribute of artificial intelligence [is that] it is foundationally reliant on resources that are owned and controlled by only a handful of big tech firms.”97

8. What are successful models of alternative ownership?

There is growing interest in alternative ownership models of digital infrastructure in Europe, and many decades of experience with community stewardship of infrastructures to draw upon. Various initiatives operate as cooperatives, municipal utilities, and open-access networks. Examples include the wireless mesh networks guifi.net in Spain and netcologne in Germany. The financial mechanisms and best practices for locally owned internet infrastructures have been documented by the Association for Progressive Communications (APC) together with Connect Humanity and Internet Society Foundation.98

Community-owned energy

Looking at the energy sector, we find many examples and policies to support community-owned infrastructures.99 In Germany these models of local ownership were established decades ago and were responsible for most of the energy systems’ decarbonization.100 The same kinds of predictable policy support that would have supported more community energy have been behind the incredibly brisk rollout of renewables in China. Only recently the economics of renewables has made it more lucrative for corporations, which is why we’ve seen a significant increase in their involvement.

Today the trends in energy and digital infrastructures are converging, so we see an opportunity to co-create these infrastructures with communities as outlined by Max Schulze with the SDIA.101

Analysis of Harms: Economic

9. How do monopolistic practices affect economies?

In recent years, the European Commissions and the US Federal Trade Commission have investigated the anticompetitive practices of tech companies with increasing scrutiny. As leading antitrust scholar Tim Wu points out, monopolies are not new. Tech companies have simply come of age in an era where antitrust has been systematically eroded.102 They have operated in a unique market environment that allows them to consolidate wealth, use the profits from one area of business to squeeze out competitors in their new “kill zones”, be that books, online ads, search, maps, cloud computing and now generative AI. They invest heavily in lobbying and because of their disproportionate resourcing, representatives from these companies can greatly outspend voices representing civil society and the public interest.

Big Tech investing in energy. It is worrying to see the same few tech companies massively invest in energy infrastructure, leveraging their influence to get access to clean energy while not doing enough to decarbonize the grid and help meet preexisting demand. For example, Amazon is building a huge data center next to a nuclear power plant in the US.103 The company does pay above wholesale rates, but still less than what consumers pay, so local communities are left relying on dirtier fossil generation at a higher price, while no new decarbonization has taken place and the usage of a nuclear plant has been extended to meet entirely new demand from Amazon’s cloud services. For its huge data center operations in Nevada, USA, Google signed agreements for geothermal energy on a tariff to primarily supply its data centers, rather than helping nearby communities decarbonize.104 These examples make clear not only of how energy intensive AI is, but how big tech companies are not doing enough taking carbon-free capacity needed elsewhere. Again we see big players, thanks to their vertical integration, bundling and anticompetitive behavior, having the capital to make infrastructure investments that smaller players cannot afford.

10. How does interoperability shift monopolistic practices and what are the benefits of that?

Interoperability in digital infrastructures can help combat monopolistic practices. It facilitates interaction across diverse platforms, which fosters competition and empowers user choice. Standardized protocols and APIs break down proprietary barriers and open doors for new services and possibilities. As digital rights activist and author Cory Doctorow argues, interoperability enables greater choice and flexibility in selecting service providers, driving down prices and improving product quality, which ultimately results in more vibrant, diverse and resilient digital ecosystems.105 By blocking interoperability, incumbent players further consolidate their power in the market.

We recommend looking at how interoperability could play out in the digital infrastructure for cloud computing. Currently many barriers are in place to switch cloud providers or to use multiple providers at once.106 These barriers include egress fees that charge customers transfer their data out of a cloud, which the hyperscalers set significantly higher than most other providers. There are also technical restrictions on interoperability imposed by the leading companies to prevent their services working effectively with services from other providers. This means customers need to put additional effort into reconfiguring their data and applications to work on different clouds. The major cloud providers lock in customers with committed spend discounts which incentivize customers to use a single hyperscaler for their cloud needs and makes it less attractive to switch to a rival provider. A regulatory requirement to interoperate would change this sector and shift power.

We see precedence in tackling monopolistic dynamics in other sectors. In the early 2000s, the European Union took significant steps to break up telecommunications monopolies and introduce competition. This included mandatory separation of former state-owned monopolists’ wholesale and retail operations, coupled with functional separation or full structural separation in some countries. As a result, 5G and fiber coverage is greater in the EU than many other regions, and there is also more competition. Importantly, in stark contrast to the US, European customers pay less per unit and get better service from their connectivity.107 Similarly, in the energy sector, the public has benefited from unbundling.108

11. What role does the government play in who can build and control digital infrastructure?

Governments regulate digital infrastructure to ensure fair competition, promote innovation, and protect citizens’ interests. In some cases, governments may also invest directly in building digital infrastructure, either independently or in partnership with private entities. Governments influence the development and implementation of digital infrastructure through policies, funding programs, and procurement decisions.

The Irish government, for example, released principles for the role of data centers in the country’s enterprise strategy. The principles included providing economic benefit and employment, renewables additionality, decarbonized data centers by design, as well as SME access and community benefits.109 In the Netherlands, there is a trend to decentralize decision-making to municipalities while the national government facilitates the building of data centers as a national industrial development plan.

Digital infrastructure investment in Germany

The German government funds the development of digital infrastructure with a variety of mechanisms. The Federal Government recently published its first Strategy for International Digital Policy to act as a compass for international digital policy and positioning of Germany.110 In the coalition agreement of the German Federal Government from 2021, the digital infrastructure was set as one of the priorities with a goal of the nationwide supply of fiber to the home and 5G networks by 2025.111

The German federal government oversees regulatory bodies like the Federal Network Agency (BNetza) and Bundesamt für Sicherheit in der Informationstechnik (BSI),112 which regulate and protect telecommunications and IT infrastructure. Both entities actively participate in setting standards, issuing guidelines, and ensuring compliance for digital infrastructures and services. The BSI furthermore stipulates how data centers should be safely built and operated.113

The Federal Ministry of Transport and Digital Infrastructure (BMDV) and the BNetzA are primarily responsible for deciding how internet infrastructure is built and deployed. The BMDV sets the strategic goals and policies for digital infrastructure114 while the BNetzA implements regulations and ensures fair competition in the telecommunications and digitalisation markets.115 Together they facilitate the deployment of high-speed broadband networks and promote digitalization across the country. Additionally, the Conference of State Ministers of Economic Affairs (WMK)116 contributes to decisions regarding internet infrastructure (data transfer and the market of the digital economy), coordinating regional efforts and aligning objectives with the federal government.

Some German governmental departments host their IT infrastructure while others rely on shared services or private hosting providers.117 The German Federal Ministry of the Interior, Building and Community (BMI) operates several data centers to support its own IT infrastructure.118

Municipal governments in Germany often do not directly control internet infrastructures for their cities. Instead, they partner with private companies to deliver internet services to residents and businesses. However, some cities have developed publicly owned networks called municipal broadband or municipality-owned WiFi networks. Examples include netcologne and the Hamburg fiber “Wilhelm Tel.”

Germany as a two-hub data center. Alongside these investments, we see Germany becoming a two-hub nation for data centers. Berlin will join Frankfurt as a major data center cluster in the continent. The German federal government regulates data center operations with the recent Energy Efficiency law119 which now sits alongside regulation at a municipal level in for example Frankfurt.120

At the European level, the European Commission plays a crucial role in establishing common policies, laws, and regulations that apply to digital infrastructure. The Body of European Regulators for Electronic Communications (BEREC) coordinates national regulators to enforce consistent telecom rules and promote fair competition.121 Recently, the European Union announced the establishment of the European Cybersecurity Industrial, Technology and Research Competence Centre, which aims to enhance cybersecurity capabilities and boost the region’s strategic autonomy in this field.122

Some European countries, including Germany, have initiated efforts to build standards and best practices for decentralized, sovereign infrastructure for data processing, storage and transfer to counterbalance the dominance of foreign providers. Open source remains a key strategy for a healthy and sovereign digital ecosystem.

Strengthening democracy by practicing democracy

The government can play a role bringing the voices of impacted communities into the decision-making process around digital infrastructure. Scholar Julia Rone makes the case for democratic engagement in digital infrastructure:

“[M]ost debates on digital sovereignty so far have overlooked the sub-national level, which is especially relevant for decision making on digital infrastructure…I insist that what matters is not only where digital sovereignty lies, that is, who has the power to decide over digital infrastructural projects…[w]hat matters is also how power is exercised. Emphasizing the popular democratic dimension of sovereignty, I argue for a comprehensive democratization of digital sovereignty policies…The shape of the cloud should be citizens’ to decide.”123

A few years ago, thanks to movement organizing and democratic engagement, the European Union rallied around an agenda for a twin transition: a just transition in energy and digital transformation. Over the last four years, this narrative has mutated from a justice-centered promise to instead call for increasing military defense, securing critical supply chains and accelerating extractivism and colonial dynamics124 even within Europe’s borders.125

Funders working in the public interest can help reclaim the justice framing for an energy transition and digital transformation and strengthen citizens’ participation in determining the future of digital infrastructure.

Acknowledgements

We would like to highlight research done by these scholars and critical friends that has informed our thinking and thank several who participated in interviews:

- Green Screen Coalition for Digital Rights and Climate Justice

- critical infrastructure lab

- The Engine Room126

- Sustainable Digital Infrastructure Alliance (SDIA)127

- AI Now128

- Digital Freedom Fund

- Environmental Law Institute

- Coalition for Independent Technology Research

- Sovereign Tech Fund

- EDRi129

- Open Markets Institute130

- Ofcom131

Thank you especially to Max Schulze for a critical reading and advice. Thank you to the Mercator team, Carla Hustedt, Lea Wulf and Elisabeth Nöfer, for your collaboration and thoughtful input. Green Web Foundation colleagues Chris Adams and Hannah Smith, thank you for your contributions and support on this report!

Suggested citation

Thorne, M. (2024): Critical Dependencies: How power consolidation of digital infrastructures threatens our democracies—and what we can do about it. Green Web Foundation. https://www.thegreenwebfoundation.org/publications/report-critical-dependencies/

This report is made available under a Creative Commons Attribution 4.0 International (CC BY SA 4.0) license. For media or other inquiries please get in touch.

Footnotes

- Professor Leah Stokes first coined the term “fog of enactment” in her book Short Circuiting Policy: Interest Groups and the Battle Over Clean Energy and Climate Policy in the American States, Studies in Postwar American Political Development (New York, 2020; online edn, Oxford Academic, 23 Apr. 2020), https://doi.org/10.1093/oso/9780190074258.001.0001. Her research focused on understanding the strategies used by incumbents in the energy sector to protect their business models, frequently at the expense of equity and sustainability. The Green Web Foundation explored this concept applied to the digital sector: https://www.thegreenwebfoundation.org/publications/report-fog-of-enactment/ ↩︎

- Large tech firms spent about €113m in lobbying in the EU in 2021, outspending every other industry. https://corporateeurope.org/en/2023/09/lobbying-power-amazon-google-and-co-continues-grow ↩︎

- Tech company expenditure and influence in academic research is significant. Furthermore, they control almost all major industry associations which are supposed to work on behalf of ‘all of their members’/’represent European interests’, including: Digital Europe, Digital4SME, EUDCA, DDA, DCA (UK), Eco Verband, BITKOM and more. ↩︎

- Example of Sweden subsidizing data centers (and rolling it back): https://www.tillvaxtanalys.se/in-english/publications/wp/wp/2024-02-02-assessing-the-welfare-effects-of-electricity-tax-exemptions-in-general-equilibrium-the-case-of-swedish-data-centers.html ↩︎

- Reed, Bill (2007). Shifting from ‘sustainability’ to regeneration, Building Research & Information, 35:6, 674-680, DOI: https://doi.org/10.1080/09613210701475753 ↩︎

- We refer to a “digital product” as a product that only exists in virtual form, for example software as a service. It runs on “digital resources,” which are the smaller computational units needed to make a digital product work. Compare this to “digitalization,” which is about transforming existing (often physical) products by integrating digital capabilities, such as a car running on a software operating system. Digital products are often used to transform non-digital things into digital ones, and they therefore require digital resources to work. Owners of digital infrastructure are in the business of generating digital resources, and they use those resources to power their own digital products or they sell the resources to clients to power other products. ↩︎

- Statista. (2023). Worldwide market share of leading cloud infrastructure service providers in 2021. Statista. [Graph]. https://www.statista.com/chart/18819/worldwide-market-share-of-leading-cloud-infrastructure-service-providers/ ↩︎

- Centre for International Corporate Tax Accountability and Research. (2022). Microsoft: Gaming Global Taxes, Winning Government Contracts. https://cictar.org/all-research/microsoft ↩︎

- Alphabet funded SIP (an infrastructure investment fund) points at the problem: https://www.datacenterflexibility.com/ ↩︎

- Top public purchase agreement buyers in 2023 according to BNEF: https://about.bnef.com/blog/corporate-clean-power-buying-grew-12-to-new-record-in-2023-according-to-bloombergnef/ ↩︎

- For example loadshedding in South Africa prioritizing electricity to data centers over homes: Ndiwalana, Samantha. (2024, February 1). A people-centred approach to thinking about data centres in South Africa. The Green Web Foundation. https://www.thegreenwebfoundation.org/news/a-people-centred-approach-to-thinking-about-data-centres-in-south-africa/ ↩︎

- In the example of Germany, its Foundational Laws (Grundgesetze) stipulates that: “Property entails obligations. Its use shall also serve the public good”. This legal framework opens the door to aligning the purpose of digitalization with societal good rather than shareholder profit. ↩︎

- Riofrancos, Thea. (2020, August 27). We Can’t Talk About Tech Without Talking About Resources [Audio podcast episode]. In Tech Won’t Save Us. https://techwontsave.us/episode/24_we_cant_talk_about_tech_without_talking_about_resources_w_thea_riofrancos.html ↩︎

- “Acting at the Intersections of Climate, Technology and Philanthropy” during the Environmental Grantmakers Association (https://ega.org/), 2024. ↩︎

- Ofcom. (2023). Cloud services market study: Final report. https://www.ofcom.org.uk/internet-based-services/cloud-services/cloud-services-market-study/ ↩︎

- See for example https://carbontxt.org/, an open convention piloted by the Green Web Foundation to support a commons of financial and sustainability data. ↩︎

- Kak, A., & West, S. M. (2023, April 11). AI Now 2023 landscape: Confronting tech power. AI Now Institute. https://ainowinstitute.org/2023-landscape ↩︎

- For example, following a model from the US, the public could benefit from an intervener compensation program for regulated monopolies. This makes money available for specialized skilled people to argue on behalf of a community for disputes. ↩︎

- Access Now. (2023, October 12). Joint Statement: Internet Governance Forum must reverse decision to make Saudi Arabia its next host. https://www.accessnow.org/campaign/igf-reverse-saudi-arabia-host-decision/ ↩︎

- Other promising approaches include the Make Amazon Pay campaign, which resulted in Amazon lobbyists being barred from European Parliament. Groups like Digital Freedom Fund are doing essential tech policy and strategic litigation with an intersectional approach, for example combatting surveillance in a way that centers the needs and experiences of migrants and marginalized communities. ↩︎

- In France, funding for mobility alternatives such as electric cargo bikes came from passing energy efficiency laws that created a redistributive mechanism for the profits of the energy sector, a regulated monopoly. Now France is the leader for active transport for fossil-free last mile delivery. ↩︎

- Caramizaru, A., & Uihlein, A. (2020). Energy communities: An overview of energy and social innovation (EUR 30083 EN). Publications Office of the European Union. https://publications.jrc.ec.europa.eu/repository/bitstream/JRC119433/energy_communities_report_final.pdf ↩︎

- There is a differentiated point to be made that one could unbundle cloud services/infrastructure itself, e.g. giving clients the ability to run an AWS service with resources provided by another provider such as Hetzner, OVH or Green Host. This could also work, albeit on a much smaller scale and will likely not have an effect on the sheer size of the digital conglomerates. ↩︎

- European Commission. (2021). Third Energy Package. https://energy.ec.europa.eu/topics/markets-and-consumers/market-legislation/third-energy-package_en ↩︎

- Informed by https://sdialliance.org/about/ and Max Schulze. ↩︎

- United Nations Secretary-General’s Roadmap for Digital Cooperation. (2020). United Nations. https://www.un.org/en/content/digital-cooperation-roadmap/ “Half of the world’s population currently does not have access to the Internet. By 2030, every person should have safe and affordable access to the Internet, including meaningful use of digitally enabled services in line with the Sustainable Development Goals.” ↩︎

- International Telecommunication Union. (2024, April 21). Connect 2030 – An agenda to connect all to a better world. ITU. https://www.itu.int/en/mediacentre/backgrounders/Pages/connect-2030-agenda.aspx ↩︎

- United Nations Human Rights Council. (2021, July 7). The promotion, protection and enjoyment of human rights on the Internet (A/HRC/47/L.22). https://ap.ohchr.org/documents/dpage_e.aspx?si=A/HRC/47/L.22 ↩︎

- Germany is one of the pioneers of energetically-self-reliant connectivity. For example, once deployed, this station will never need fossil fuels to provide connectivity: https://www.datacenterdynamics.com/en/news/o2-telefonica-builds-self-sufficient-off-grid-5g-tower-in-germany/

One of the key changes in the shift to 5G is that it can support a shift from a single monolithic “stack” of technology to a more unbundled setup with a network of actors. Green Web Fellow Kevin Webb explored this in in his project: https://www.thegreenwebfoundation.org/news/putting-the-internet-back-in-the-things/ ↩︎ - Much of this report focuses on digital infrastructure needed for data processing, storage and transfer. Less attention has been given to the infrastructure needed internet access, although this is a societally important aspect. ↩︎

- Resources on how to run citizen assemblies including virtually prepared by MySociety: https://www.mysociety.org/2020/06/30/citizens-assemblies-are-back-in-handbook-form/ ↩︎

- The practice of citizen assemblies is well established in European countries like Ireland: https://www.citizensinformation.ie/en/government-in-ireland/irish-constitution-1/citizens-assembly/ and are being explored in Germany (Bürgerräte): https://www.bundestag.de/buergerraete ↩︎

- Schulze, M., Kumar, R., and Oghia, M (2022), ‘Taxonomy Guide: Infrastructure in the Digital Economy’, Trade Competitiveness Briefing Paper 2022/01, Commonwealth Secretariat, London. https://www.thecommonwealth-ilibrary.org/index.php/comsec/catalog/book/952?ref=maxschulze.com. ↩︎

- S12Y Wiki. A project from Leitmotiv and part of the Sustainable Digital Products Program, initiated as part of the SoftAWERE Project by the SDIA & German Environmental Protection Agency with launch funding from the German Ministry of Economic Affairs and Climate Protection. https://s12y.wiki/getting-started/definitions/#digital-product ↩︎

- Schulze, M. (2022), “Untangling digital infrastructure: A new school of thought.” Presentation, EU Connect, 28th of September 2022. https://www.maxschulze.com/content/files/2023/07/2022-09-28-EU-Connect-University-Slides.pdf ↩︎

- Statista. (2023). Worldwide market share of leading cloud infrastructure service providers in 2021. Statista. [Graph]. https://www.statista.com/chart/18819/worldwide-market-share-of-leading-cloud-infrastructure-service-providers/ ↩︎

- Autorité de la concurrence. (2023). Cloud computing: Authorité de la concurrence publishes its market study on competition in cloud computing. https://www.autoritedelaconcurrence.fr/en/press-release/cloud-computing-autorite-de-la-concurrence-issues-its-market-study-competition-cloud ↩︎

- SRG Research. (2023). Hyperscale data center capacity to almost triple in next six years driven by AI. SRG Research. https://www.srgresearch.com/articles/hyperscale-data-center-capacity-to-almost-triple-in-next-six-years-driven-by-ai ↩︎

- SRG Research. (2023). On premise data center capacity being increasingly dwarfed by hyperscalers and colocation companies. SRG Research. https://www.srgresearch.com/articles/on-premise-data-center-capacity-being-increasingly-dwarfed-by-hyperscalers-and-colocation-companies ↩︎

- Ofcom. (2023). Cloud services market study: Final report. https://www.ofcom.org.uk/internet-based-services/cloud-services/cloud-services-market-study/ ↩︎

- The Register (2024, May 1). “AWS hits $100B revenue run rate, expands margins, delivers most of Amazon’s profit” https://www.theregister.com/2024/05/01/amazon_q1_2024/ ↩︎

- SRG Research. (2023). European cloud providers continue to grow but still lose market share. SRG Research. https://www.srgresearch.com/articles/european-cloud-providers-continue-to-grow-but-still-lose-market-share ↩︎

- Synergy Research Group. (2024, February 1). Cloud Market Gets its Mojo Back; AI Helps Push Q4 Increase in Cloud Spending to New Highs. https://www.srgresearch.com/articles/cloud-market-gets-its-mojo-back-q4-increase-in-cloud-spending-reaches-new-highs ↩︎

- Statista. (2024). Public Cloud – Europe. https://www.statista.com/outlook/tmo/public-cloud/europe ↩︎

- Autorité de la concurrence. (2024, April 1). Cloud computing: the Autorité de la concurrence issues its market study on competition in the cloud sector. https://www.autoritedelaconcurrence.fr/en/press-release/cloud-computing-autorite-de-la-concurrence-issues-its-market-study-competition-cloud ↩︎

- ReportLinker (2022). European Telecom Trends in 2022. https://www.reportlinker.com/clp/global/8615 ↩︎

- Mordor Intelligence. (2024). Germany Telecom Market Share. https://www.mordorintelligence.com/industry-reports/germany-telecom-market/market-share ↩︎

- Mordor Intelligence. (2023). Germany Telecom Market – Industry Analysis, Share, Trends, Size, Competitive Landscape and Forecast 2021-2026. Mordor Intelligence. https://www.mordorintelligence.com/industry-reports/germany-telecom-market ↩︎

- Mordor Intelligence. (2024). Germany Data Center Networking Market Size & Share Analysis – Industry Research Report – Growth Trends. https://www.mordorintelligence.com/industry-reports/germany-data-center-networking-market ↩︎

- International Energy Agency. (2024). Average lead times to build new electricity grid assets in Europe and the United States, 2010-2021 [Chart]. IEA. https://www.iea.org/data-and-statistics/charts/average-lead-times-to-build-new-electricity-grid-assets-in-europe-and-the-united-states-2010-2021 ↩︎

- Hintemann, R., Hinterholzer, S., Graß, M., & Grothey, T. (2022). Bitkom-Studie: Rechenzentren in Deutschland 2021 – Aktuelle Marktentwicklungen. Bitkom e.V. https://www.bitkom.org/sites/main/files/2022-02/10.02.22-studie-rechenzentren.pdf ↩︎

- Federal Trade Commission. (2024, March 29). Generative AI Raises Competition Concerns. https://www.ftc.gov/policy/advocacy-research/tech-at-ftc/2023/06/generative-ai-raises-competition-concerns ↩︎

- OfCom. (2023). Cloud services market study: Final report. https://www.ofcom.org.uk/internet-based-services/cloud-services/cloud-services-market-study/ ↩︎

- Autorité de la concurrence. (2023). Cloud computing: Authorité de la concurrence publishes its market study on competition in cloud computing. https://www.autoritedelaconcurrence.fr/en/press-release/cloud-computing-autorite-de-la-concurrence-issues-its-market-study-competition-cloud ↩︎

- How do the large providers consolidate their position? Hyperscale data centers are expensive to deploy but very profitable to run. They only need to sell around 25% of their own capacity to break even. This means they can offer the other 75% of the data center capacity at any price and still make money. Or they can offer that extra capacity for free while competitors go under.

Alternatively, they can reinvest the profits from sales on the 75% of capacity into deploying a new hyperscale data center, which in turn only needs to sell 25% of its own capacity to break even. Each time they do this, they end up with even more spare capacity they can use against competitors.

For the very large companies, they can cross-subsidize these investments. Google has search, Microsoft has its office suite, and Amazon has retail, etc. All those businesses make money that they can use to generate extra data center capacity ↩︎ - Forty-one signatories from cloud computing CEOs and associations. (2022 February 7) Open letter: Why the DMA does not (yet) safeguard the EU’s cloud market https://cispe.cloud/website_cispe/wp-content/uploads/2022/02/CISPE_Vestager.letter-FINAL.pdf ↩︎

- Ritchie, H., & Roser, M. (2020). Global Aviation Emissions. Our World in Data. Retrieved from https://ourworldindata.org/global-aviation-emissions ↩︎

- International Energy Agency (2024). “Electricity 2024: Analysis and Forecast to 2026”. https://iea.blob.core.windows.net/assets/ddd078a8-422b-44a9-a668-52355f24133b/Electricity2024-Analysisandforecastto2026.pdf ↩︎

- Kamiya, G. and Bertoldi, P., Energy Consumption in Data Centres and Broadband Communication Networks in the EU, Publications Office of the European Union, Luxembourg, 2024, doi:10.2760/706491, JRC135926. https://publications.jrc.ec.europa.eu/repository/handle/JRC135926 ↩︎

- Kamiya, G. and Bertoldi, P., Energy Consumption in Data Centres and Broadband Communication Networks in the EU, Publications Office of the European Union, Luxembourg, 2024, doi:10.2760/706491, JRC135926. https://publications.jrc.ec.europa.eu/repository/handle/JRC135926 ↩︎

- International Energy Agency. (2022). Data Centres and Data Transmission Networks. International Energy Agency. https://www.iea.org/energy-system/buildings/data-centres-and-data-transmission-networks ↩︎

- ITU, Greenhouse gas emissions trajectories for the information and communication technology sector compatible with the UNFCCC Paris Agreement, 2020, p.1 https://www.itu.int/rec/T-REC-L.1470 and https://www.itu.int/en/ITU-D/Environment/Pages/Publications/Measuring-Emissions-and-Energy-Footprint-ICT-Sector.aspx ↩︎

- International Energy Agency (2024). “Electricity 2024: Analysis and Forecast to 2026”. https://iea.blob.core.windows.net/assets/ddd078a8-422b-44a9-a668-52355f24133b/Electricity2024-Analysisandforecastto2026.pdf ↩︎

- International Energy Agency (2024). “Electricity 2024: Analysis and Forecast to 2026”. https://iea.blob.core.windows.net/assets/ddd078a8-422b-44a9-a668-52355f24133b/Electricity2024-Analysisandforecastto2026.pdf ↩︎

- Hogan, M. (2015). Data flows and water woes: The Utah Data Center. Big Data & Society, 2(2). https://doi.org/10.1177/2053951715592429 ↩︎

- Mytton, D. Data centre water consumption. npj Clean Water 4, 11 (2021). https://doi.org/10.1038/s41545-021-00101-w ↩︎

- Dentons. (November 2023). Water usage and efficiency in German data centers: A regulatory overview. https://www.dentons.com/en/insights/articles/2023/november/22/water-usage-and-efficiency-in-german-data-centers-a-regulatory-overview ↩︎

- Li, P., Yang, J., Islam, M. A., & Ren, S. (2023). Making AI less” thirsty”: Uncovering and addressing the secret water footprint of ai models. arXiv preprint https://arxiv.org/abs/2304.03271 ↩︎